Most people keep their money in a bank, but there has been a significant shift in the type of bank. Many (77 percent) still rely on traditional banks to hold all or some of their funds, but they are not too happy with them. Thirty-five percent prefer digital banks as their primary service provider, and the numbers are growing. The forecast for the digital banking market in Canada, which includes online-only banks, is a 13.1 percent rise from 2021 to 2026.

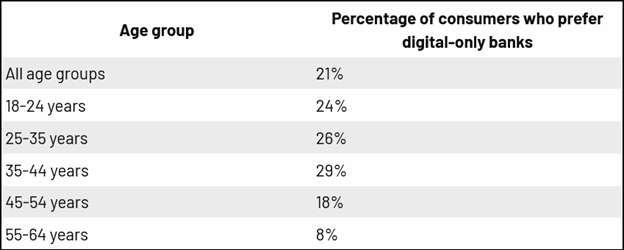

Of particular note is the interest in digital-only banks among younger people.

Traditional banks offer online banking services, but digital-only banks have no physical presence. Consumers transact exclusively online using a virtual debit card on the app. You can use a virtual debit card pretty much the same way as a physical card, except for the ability to use the ATM.

Some digital-only banks also offer add-on features to make it even more attractive to consumers. One of these add-ons is cash-back debit cards.

Don’t miss: Cash app paper money deposit not showing up

Cash-Back Debit Cards Explained

Most people are familiar with cash-back credit cards. As the name implies, cardholders earn cash back for some or all their transactions using that credit card. Some people use their credit cards for that reason without realizing they are spending more than they should.

Cash-back debit cards work somewhat the same way. They allow account holders to get back some of the money they spend daily. However, they can only spend the money they have in the account.

Many digital banks credit back one percent of an eligible purchase to a debit account right off the bat. Some may offer higher cash-backs when you buy from specific merchants or sign up for special account plans. However, you should know that some cash-back debit cards limit what you can get back from your purchases. They may also impose conditions for earning the cash back, such as maintaining a minimum daily balance.

You can typically sign up for cash-back debit cards without payment or service fees. However, some banks may offer tiered pricing so accountholders can get better perks, such as higher cash-back.

Are cash-back cards worth it if you have to pay for it? They are a viable option for credit cards that offer cash-backs and rewards if you want to avoid overspending. However, suppose you have reasonable control over your budget and pay your bills on time and in full. A cash-back debit card is still a good option, depending on other features offered and your financial needs and goals.

Features You Want in a Cash-Back Debit Card

Many digital banks offer cash-back for their debit cards, but the conditions vary. When choosing a cash-back debit card, find out the conditions that go with it. Only then can you determine which card checks all your financial boxes and are worth getting.

Cash-back percentages

Most digital banks offer free cash-back debit cards at one percent for eligible purchases, typically gas and groceries. Many have cash-back partners where you can get higher cash-back percentages for purchases, ranging from 2 to 10 percent.

Limitations

Some banks impose conditions for earning cash back from your debit card. It may be maintaining a minimum balance or capping the amount you can get back monthly. Sometimes, it only offers cash-back for specific merchants.

Monthly fees

Some digital banks will have tiered plans that allow you to earn cash back from more establishments, at higher rates, or both. They typically charge a small monthly fee, including other benefits, such as earning interest on your balance. A few may also offer lines of credit to help build your credit. That alone might make the monthly fee worth it if you want better credit.

Cash-back debit cards may also come with transfer and foreign exchange fees. Review the benefit checklist to determine if that is the case for a particular card or plan.

These factors can affect your overall financial benefit significantly. Let’s say you get a card with a cash-back rate of one percent for gas and groceries on a free account. However, signing up for a paid version allows cash back for food and drink. Suppose you spend $500 monthly on gas and groceries and $500 on eating out. You can only get $5 back from gas and groceries with a free account. With a paid account, you can get $10 back, more than the $4 or $5 monthly fee.

Additionally, some cash-back debit cards earn interest on the balance. For example, Canada-based Koho offers a free account where you can earn three percent interest on the balance. However, you can get five percent on its paid Essential plan. Suppose you regularly maintain $1,000 on your debit account. You will receive $30 on interest alone on the free version and $50 on the paid plan. However, some banks require you to maintain a minimum daily balance before you start earning interest.

You should also know that you cannot use virtual cash-back debit cards. However, some digital-only banks allow their customers to request a physical card. You may have to wait several days to get it, but you can use it at an ATM.

The best thing about digital banks is that if you open an account and don’t like the experience, you can close it anytime.

Applying for a Cash-Back Debit Card

Nothing can be easier than getting a cash-back debit card. Like physical debit cards, they are tied to a savings or checking account. Most digital banks let you open an account in a few minutes and may even offer a free trial for paid plans.

Generally, you must register on the platform and provide personal information, including a government ID. You may also need to put money in, usually $25, although some banks do not require it. Once the bank accepts your application, you will get a virtual debit card for transactions.

However, first things first. Before opening an account, check if the digital bank has good reviews and solid backing. Reputable digital banks have the support of a traditional bank or credit card issuer such as Visa or Mastercard. They should also have good security and deposit insurance from the federal government, such as the Canada Deposit Insurance Corporation.

Cash-Back Debit Cards vs Cash-Back Credit Cards

Comparing the benefits of debit cards vs credit cards purely on the cash-back feature is a non-starter. Credit cards allow users to spend more money than they have in their accounts, unlike debit cards. They can potentially earn more cashback from their purchases. However, that can lead to financial troubles for consumers struggling to manage their credit card debts.

From a security perspective, credit cards are typically more secure than debit cards. Most credit cards offer zero fraud liability and limit fraud losses to cardholders to $50. Debit cards also have security measures and fraud protection, but it is not all-encompassing. Visa and Mastercard provide zero liability protection for unauthorized use in Canada, so ensure your debit card enjoys that safeguard.

Takeaways

Cash-back debit cards are a good way for many to get money back from their daily purchases. Some would argue that a cash-back credit card offers more options and is more secure. However, some people do not qualify for credit cards with reasonable APRs or cannot control their spending. Because debit cards are self-limiting, no one will ever get into debt by using one.

However, not all cash-back debit card providers are created equal. You must do your due diligence and research the issuing bank’s terms, conditions, and reputation. Suppose you choose a digital-only bank to open a savings account for your spending. Ensure that it has proper backing from reputable institutions that will protect your hard-earned money from fraud and other adverse events.

My self Jean Acker, an SEO specialist. MS from the reputed college MIT. I am an innovative person, as well as have a sound interface with tech. Honestly, I easily supervise my meditations as well as my experimentation with Android and iOS.